In China, PP and PE prices have been on a downward trajectory since April, although output has remained curbed particularly since July amid producers’ efforts to bear the high production costs. Poor demand amid the ongoing covid restrictions as well as an uncertain economic outlook has been eclipsing the gradual decrease in local supply and weighing on spot prices.

Polyolefin stocks inside China remain below 700,000 tons

The two major local producers’ combined polyolefin levels were standing at/around or slightly below 900,000 tons as of late March.

Starting from late July, stock levels fell to around or slightly below 700,000 tons, which is a critical threshold suggesting that stocks are not high enough inside, and have hovered around these levels since then. This is because local producers have reduced operating rates to minimize margin losses given the persistent demand slump.

Stock levels at around 500-600,000 tons, meanwhile, imply very low stock levels inside China.

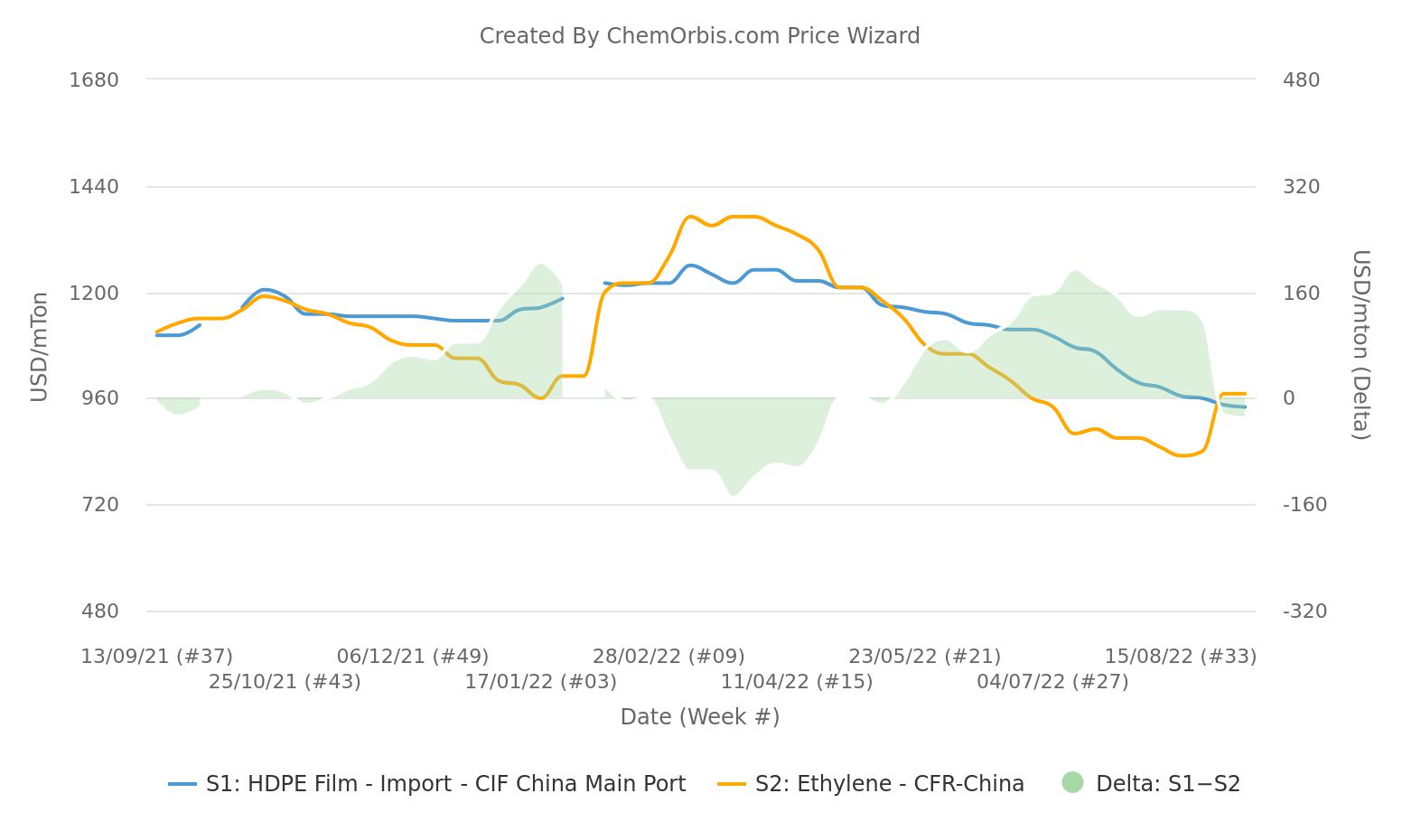

Import PE trades below spot ethylene

Run rate cuts have been applied across the production chain as cracker operators have also been lowering their operating rates to avoid the slide in monomer prices.

Taking the recent ethylene prices at $970/ton CFR NEA into account and adding a conversion cost of $200/ton on top of it, the theoretical production cost of PE comes to around $1170/ton, not including sellers’ margins.

However, current PE prices are trading almost at par with ethylene inside China and even below ethylene in the import market.

Meanwhile, local HDPE and LLDPE prices in China are standing at CNY7,845-8,350/ton, CNY7,685-7,925/ton ex-warehouse, cash inc 13% VAT during the week that ended on September 2. They come to around $1006-1071/ton, and $986-1016/ton respectively, not inc VAT, standing around $100-150/ton below the theoretical cost calculation.

In the import market, the highest HDPE and LLDPE prices are respectively reported at $930-950/ton and $910-980/ton CFR China, standing below the spot ethylene prices.

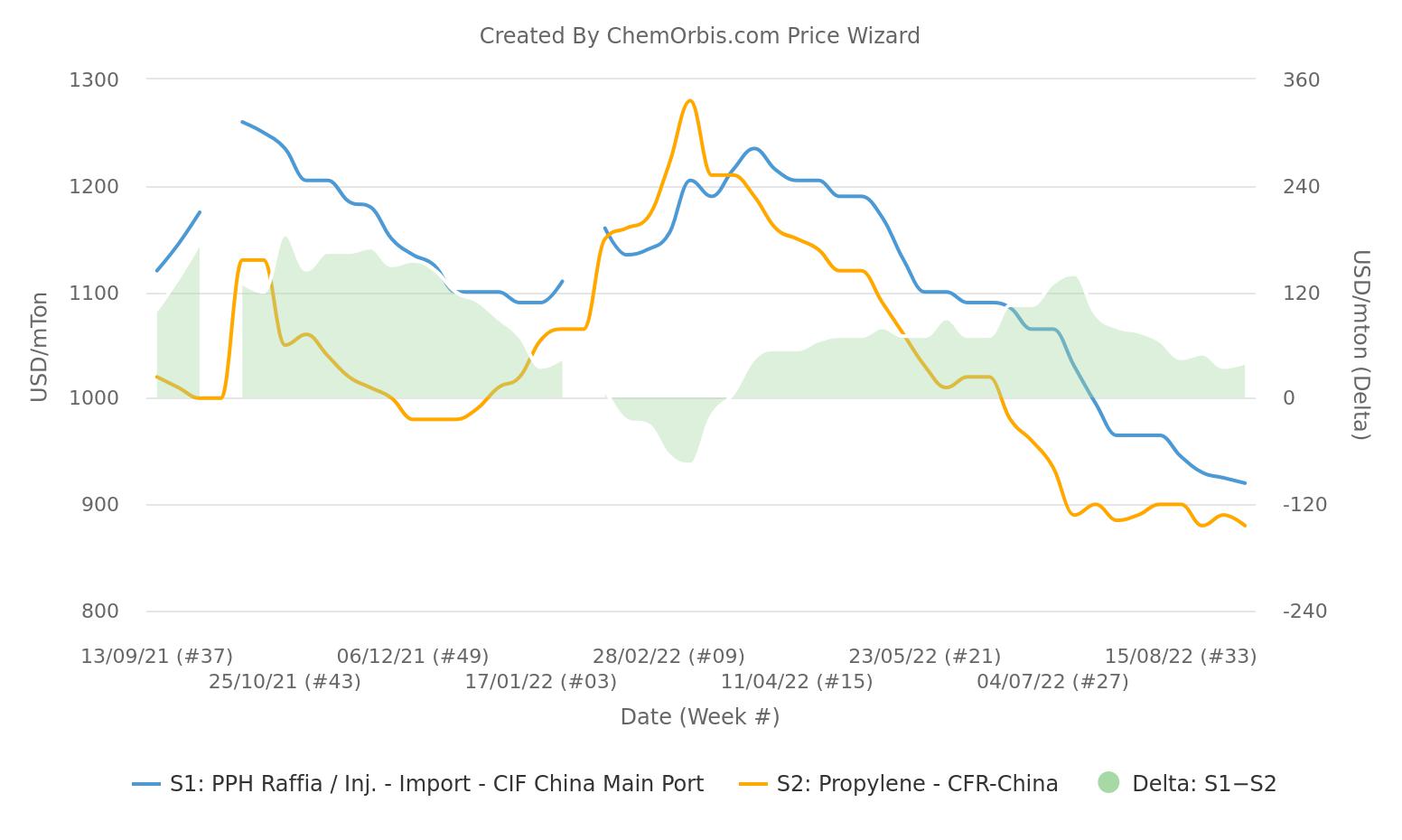

PP has a razor-thin spread to propylene

In the case of PP, the theoretical production cost corresponds to $1080/ton CFR NEA after adding an estimated conversion cost of $200/ton on top of the current propylene prices,

which are at $880/ton CFR NEA.

PP seems to be under pressure, as well, considering the razor-thin spread. The highest import homo PP raffia price reported in China is $930/ton CIF. “The prevailing market levels may be considered as the bottom, but there is no demand improvement to drive prices higher,” said a trader.

In the local market, homo PP raffia and injection prices are reported at CNY8,000-8,100/ton ex-warehouse, cash inc VAT this week, which comes to $1026-1039/ton without VAT.